60% of consumers browse merchant sites weekly. Behind the scenes, a complex web of programs and regulations keeps payments safe.

Let’s look at a customer walking into a physical retail store, trying on some jeans and tapping their card to pay. This is called a card-present transaction. Because they are physically there with their card, the transaction can be verified through methods such as chip, contactless or wallet-based authentication. These transactions have a huge success rate—about 98% of Visa card-present transactions are approved instantly.2 It’s fast, easy and reliable.

Now, imagine the customer is trying to buy the same jeans online. The customer types in their card number, hits buy and waits to see if the purchase goes through. Online shopping means the store can’t see them or their card, potentially creating additional fraud concerns related to these card-not-present (CNP) transactions.

This gap between online and offline approval rates exists because fraud is such a massive problem. Experts predict that CNP fraud could reach more than $62 billion globally by 2027.3 To help with this, issuers and merchants use strict security rules for transactions. However, sometimes, these rules block real customers by mistake. This is called a false decline—and it’s a huge issue that it is estimated will cost the global economy more than $264 billion a year by 2027.4 It’s a tough balancing act: stores want to say yes to as many good orders as possible, while declining the malicious actors.

So, what does this mean for your business? Speed is so important that more than half of shoppers (56%5) state they will choose an online store just because it offers faster payment options. If checkout takes too long, or if it asks for too much information, many people will just abandon their digital cart and go somewhere else.

And while shoppers expect a smooth experience, not all businesses can offer this just yet. Many merchants lack the right technology to support the seamless blend of digital and physical shopping. They struggle with disconnected systems, meaning their online store doesn't talk to their physical store.

Closing this technology gap is both a challenge and an opportunity for small and medium-sized businesses. Accepting online payments securely is made possible with the right support and the right solutions in place.

What are online payments?

Online payments are digital transactions that enable you to be paid for goods and services online using credit cards, debit cards, digital wallets, click-to-pay or bank transfers. These payments enable fast, secure and convenient money exchanges without the need for cash or in‑person payment processing.

How do you accept online payments?

Accepting online payments requires a secure digital infrastructure that captures various payment methods, authenticates buyers to prevent fraud and routes transactions to banks for approval. To build this experience for today's mobile-first shoppers, businesses rely on a few key technologies like the ones below:

The payment gateway

The payment gateway acts as the link between your online store and the consumer’s payment method. When a customer clicks buy, this central hub—for example, Authorize.net—securely grabs the credit card or electronic check info and passes it to the payment network to make sure the money gets where it needs to go.

Unified commerce

Unified commerce removes the friction by connecting payment systems across channels and things like loyalty programs so that at checkout, customers are able to pay, get rewards and use a discount code with minimal hassle.

Tokenization

Tokenization takes your customer’s sensitive credit card number and replaces it with a unique digital code called a token. This unique ID lets you save customers’ card details for fast, one-click buying in the future—but because the critical card data isn't stored, hackers can't steal it. When your business accepts credit card payments online, it’s a good idea to also implement tokenization as part of your strategy.

| The gateway | Unified commerce | Mobile-first browsing | Tokenization |

|---|---|---|---|

| An invisible, high-tech bridge that connects an online store to the bank. | Instead of separate, disconnected systems for payments, coupons and points, this all-in-one experience mixes everything into one smooth journey. | The growth of mobile commerce allows anytime shopping on your phone. | Takes your sensitive credit card number and replaces it with a unique digital code called a token. |

| When you click buy, this central hub—for example, Authorize.net—securely grabs your credit card or electronic check info and runs it across the bridge to the payment network. | Unified commerce removes the friction (the annoying parts of shopping). | With mobile-first browsing, shoppers use their phones to scroll through stores and build their digital shopping carts. | This unique ID lets customers save their info for fast, one-click buying in the future. |

| The gateway makes sure the money gets where it needs to go. | This approach means you can pay, get your rewards, and use a discount code all at the same time without any hassle. | Shoppers often build carts or browse even if they decide to finish buying the items later, including on a laptop or tablet. | Because the real card numbers aren’t stored, hackers can't steal them. |

What can you do to enable online payments?

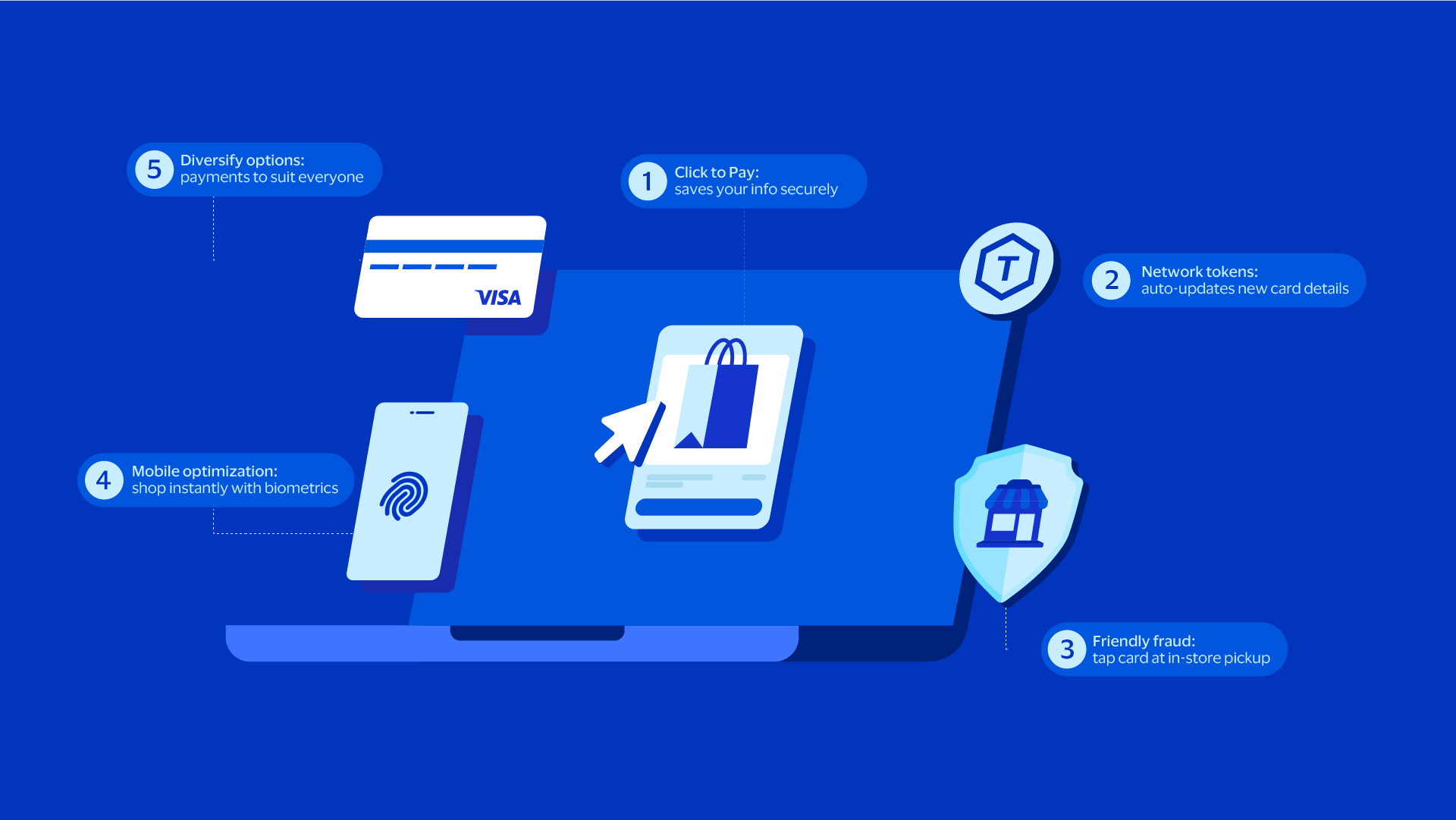

Enable Click to Pay

Securely save customers’ information so they don't have to enter it every time they make a purchase, making checkout fast. This stops shoppers from getting frustrated and abandoning their cart before hitting buy and completing their journey.

Network tokens

Card networks replace card numbers with a digital token that automatically updates behind the scenes if card details change. This keeps on-file payment details fresh, so recurring bills don't fail—and repeat purchases go through smoothly.

In-store pickup with a physical card requirement

To bridge the gap between buying online and in-store pickup, stores can ask customers to tap their physical card when they collect their items.

Diversify options

By offering a selection of payment options, merchants give customers the freedom to choose the method they trust most. Whether it is a digital invoice sent to email or a specific wallet app, giving people what they want helps a business reach new customers and keeps everyone happy.

FAQs

For smaller businesses, simpler is better. Many start by selling on marketplaces that handle the heavy lifting from a technology perspective and bring in customers. If you have your own website, use a simple plug-and-play gateway that connects easily to the bank. To make buying fast, add Click to Pay to fill in payment info automatically so customers don’t abandon their purchase.

The key rule is called PCI DSS, which is a global security framework designed to protect credit and debit card data. The best trick? Don't touch the data. Use a compliant payment provider, so card data never touches your business systems.

For subscriptions that are processed on a regular basis, like gym memberships, you can use network tokens. Unlike a plastic card that expires or gets lost, these digital tokens update automatically behind the scenes. This stops payments from failing when a customer does something like getting a new card. Alternatively, Account Updater from Authorize.net automatically updates the customer’s card details in the background, so their subscription keeps running forward. This means fewer failed payments and less involuntary churn for your business.

Think of the payment provider (gateway) as the digital cash register, securely capturing your customer’s card details to send off for approval. The processor moves the money, talking to the card networks and banks to verify the transaction and settle the funds into your account. Many modern services bundle both together. But larger merchants might use one gateway to connect to different processors to find better rates or improve approval rates.

Small and medium-sized businesses should focus on what affects your bottom line: fraud and chargeback rates, authorization rate, settlement speed, and cost. SMBs should look for simple providers to avoid managing complex integrations. Don’t just chase the lowest transaction fee but look at what else comes in the box. Does the provider offer effective fraud management tools, built in invoicing, account updater or elements that help you run faster like Tap to Pay? Look for tools that save you time and money, so you can focus on what you do best—running your business.

A payment gateway (such as Authorize.net) works like a middleman—sitting at the heart of the payments process connecting all the key players. These include the customer, the store owner, the issuer (customer’s bank) and the acquirer (merchant’s bank). When your business uses a payment gateway, it can process and accept payments, while also accessing services like transaction management, reporting and billing. If your business has a physical storefront, you can use the gateway to process CP payments at checkout terminals or via mobile devices around the store. If you have a website then accepting payments online is just as easy, whether via credit cards or other methods, such as eChecks.

How soon you can start accepting payments depends on factors like how quickly your payment gateway can approve your account and whether you have a merchant account already, which is needed to accept credit cards. A payment gateway such as Authorize.net can approve your account upon successful completion of an application, then your business can be ready to start accepting payment in just a few minutes by updating your payment gateway with the parameters provided by your merchant provider. All-in-one accounts include a merchant account, and these can take up to five business days to open—depending on variables like the account holder’s credit history or what industry they work in.

Start accepting payments today

- PYMNTS Intelligence. "2025 Global Digital Shopping Index."

- Visa. "Gross Approval Rate from Global Risk Team" Global Authorization Trends Tracker, 2024.

- Juniper Research. “Online Payment Fraud. Emerging Threats, Segment Analysis & Market Forecasts 2022-2027”.

- Datos Insights. "The Future of E-Commerce: Innovations to Protect and Enrich the Online Channel", August 2024, https://globalclient.visa.com/datospaper.

- Visa & PYMNTS. “2025 Global Digital Shopping Index”, February 2025.

- Visa Acceptance Solutions, Cybersource, The Merchant Risk Council (MRC), Verifi, and B2B International. "2025 Global eCommerce Payments & Fraud Report", 2025, https://www.visaacceptance.com/content/dam/documents/campaign/fraud-report/global-fraud-report-2025.pdf

Disclaimer: Case studies, comparisons, statistics, research, and recommendations are provided “AS IS” and intended for informational purposes only and should not be relied upon for operational, marketing, legal, technical, tax, financial or other advice. Visa neither makes any warranty or representation as to the completeness or accuracy of the information within this document, nor assumes any liability or responsibility that may result from reliance on such information. The information contained herein is not intended as investment or legal advice, and readers are encouraged to seek the advice of a competent professional where such advice is required.